Introduction

When searching for the best personal loan rates in the USA, one of the biggest decisions borrowers face is choosing between traditional banks and online lenders. Both options offer personal loans—but the difference in interest rates, approval speed, and eligibility can significantly impact how much you pay.

So, which one is better in 2026?

This guide provides a detailed comparison of personal loan rates (banks vs online lenders), helping you understand where you can get the lowest rates, fastest approval, and best overall deal.

Overview: Banks vs Online Lenders

Before comparing rates, it’s important to understand how these two types of lenders operate.

Traditional Banks

Banks are well-established financial institutions offering loans through branches and online platforms.

Best for:

- Borrowers with strong credit

- Large loan amounts

- Long-term financial relationships

Online Lenders

Online lenders are digital-first financial companies that offer fast, paperless loan processes.

Best for:

- Quick approvals

- Borrowers with fair or limited credit

- Flexible loan requirements

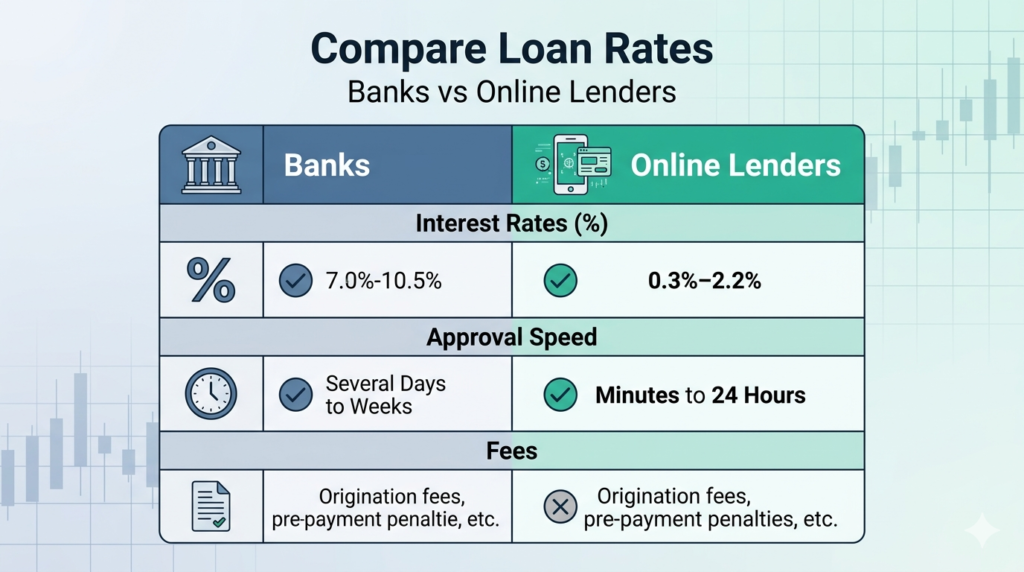

Personal Loan Interest Rates Comparison (2026)

Here’s a clear comparison of average personal loan rates in the USA:

| Loan Type | Interest Rate (APR) | Credit Requirement | Funding Speed |

|---|---|---|---|

| Banks | 7% – 13% | High (700+) | 2–7 days |

| Online Lenders | 6% – 36% | Flexible | 1–3 days |

Key Insight:

- Banks generally offer lower interest rates for qualified borrowers.

- Online lenders offer wider rate ranges due to flexible approval criteria.

Detailed Comparison: Banks vs Online Lenders

1. Interest Rates

Banks

- Typically offer lower starting APRs (7%–13%) for excellent credit borrowers

- Relationship discounts available for existing customers

- Secured loans can reduce rates further

Online Lenders

- Rates range from ~6% to 35%+ depending on credit

- Higher rates for lower credit scores

- More transparency with rate comparison tools

👉 Verdict:

- Best rates → Banks

- More approval flexibility → Online lenders

2. Approval and Funding Speed

Banks

- Slower approval due to manual underwriting

- Funding time: 2–7 business days

- May require in-person verification

Online Lenders

- Instant or same-day approval possible

- Funding within 24–72 hours

- Fully digital process

👉 Verdict:

- Fastest option → Online lenders

3. Eligibility Requirements

Banks

- Require:

- High credit score (usually 700+)

- Stable income

- Low debt-to-income ratio

Online Lenders

- Accept:

- Fair or even poor credit

- Thin credit history

- Use alternative data (AI-based underwriting)

👉 Verdict:

- Easier approval → Online lenders

4. Fees and Charges

Banks

- Lower or negotiable fees

- Fewer hidden charges

- Often no origination fee for premium customers

Online Lenders

- Origination fees can go up to 8%–12% in some cases

- Late fees may apply

👉 Verdict:

- Lower fees → Banks

5. Loan Flexibility

Banks

- Fixed loan structures

- Limited customization

Online Lenders

- Flexible loan purposes

- Adjustable repayment terms

- Prequalification without affecting credit score

👉 Verdict:

- More flexibility → Online lenders

Real-World Rate Examples (2026)

Here are typical personal loan rates based on credit score:

| Credit Score Range | Average APR |

|---|---|

| 720+ | 7% – 10% |

| 660–719 | 12% – 18% |

| Below 660 | 20%+ |

👉 Lower credit = higher rates regardless of lender type

Pros and Cons Comparison

Banks

Pros:

- Lower interest rates

- Trusted institutions

- Lower fees

Cons:

- Strict eligibility

- Slower approval

- Less flexibility

Online Lenders

Pros:

- Fast approval (instant decisions)

- Easy online application

- Flexible credit requirements

Cons:

- Higher interest rates (for many borrowers)

- Possible origination fees

- Less personal support

Which Option is Better for You?

Choose a Bank If:

- You have excellent credit (700+)

- You want the lowest interest rate

- You don’t need urgent funds

Choose an Online Lender If:

- You need quick cash

- Your credit score is fair or low

- You want a simple online process

Expert Tips to Get the Lowest Rates

To secure the best personal loan rates in the USA:

- Improve your credit score before applying

- Compare at least 3–5 lenders

- Use prequalification tools

- Reduce your debt-to-income ratio

- Choose shorter repayment terms

Common Mistakes to Avoid

- Not comparing banks and online lenders

- Ignoring origination fees

- Applying without checking credit score

- Choosing longer terms without understanding total cost

- Falling for “instant approval” without reading terms

FAQs

1. Are bank loans always cheaper than online lenders?

Generally yes, but only for borrowers with strong credit profiles.

2. Do online lenders have higher interest rates?

Yes, especially for borrowers with lower credit scores.

3. Which is faster: banks or online lenders?

Online lenders are significantly faster, often funding within 1–3 days.

4. Can I get a low interest rate online?

Yes, if you have excellent credit, online lenders can offer competitive rates starting around 6%.

5. Do banks charge fewer fees?

Typically yes, especially for existing customers.

6. Which is safer: bank or online lender?

Both are safe if you choose reputable lenders.

Conclusion

When comparing personal loan rates in the USA, the choice between banks and online lenders depends on your priorities.

- If your goal is lowest interest rates → choose banks

- If your goal is fast approval and easy access → choose online lenders

The smartest strategy is to compare both options before applying. Even a small difference in interest rate can save you thousands over time.

Disclaimer

This article is for informational purposes only and does not constitute financial advice. Loan rates, terms, and eligibility vary by lender and borrower profile. Always review official terms and consult a financial advisor before applying.